Q3 2023 Market Update

MEET JIM STADLER, OUR PROCUREMENT EXPERT.

Jim is Vice President of Estimating and Purchasing at Commodore Builders. He brings over 20 years of experience working across all our markets including Life Sciences, Public and Municipal, Corporate Interiors, Commercial, and Institutional. His deep knowledge of costs during preconstruction planning helps to guide our teams through the cost planning process. Jim holds a B.S. in Civil Engineering from Norwich University.

Q3 2023 Market Analysis | Where we are today

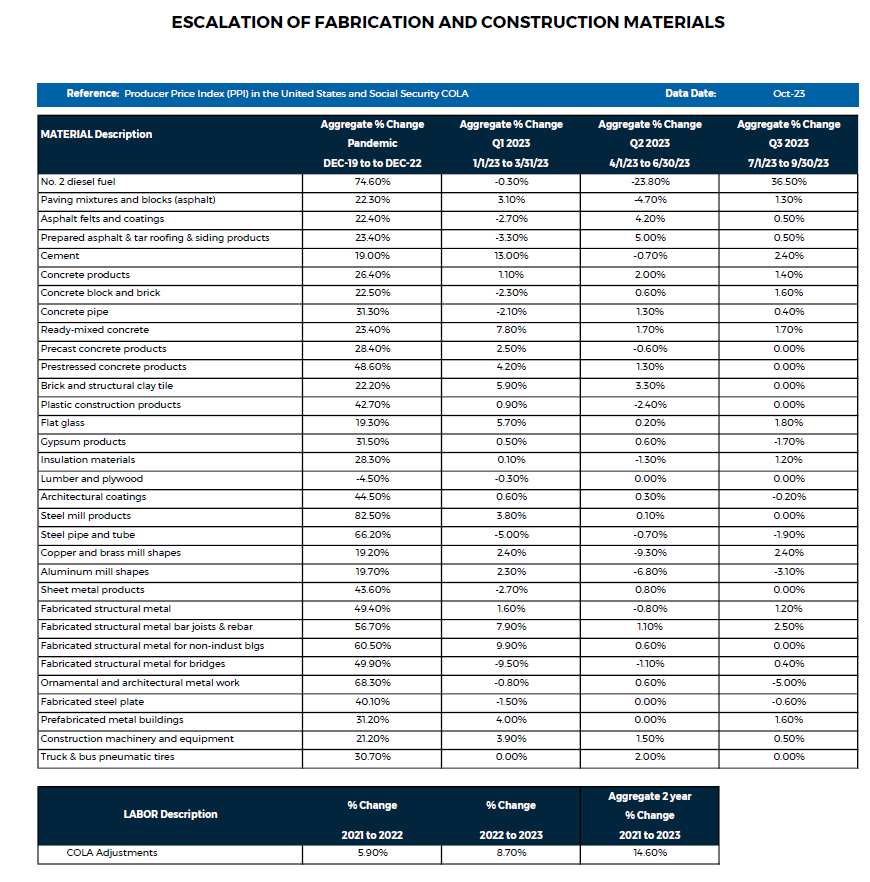

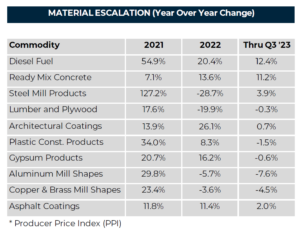

Material prices were flat in Q3 compared to Q2, and are expected to continue on this trend for the balance of 2023 and into 2024 in response to weaker demands, higher interest rates, and improving supply chain conditions. The Consumer Price Index (CPI) rate reached 3.7% in August 2023, which is more in line with the 40-year average of 3.8%, and down significantly from the 40-year high of 9.1% from June of 2022. The U.S. Bureau of Labor and Statistics reports that the construction industry labor force increased by 4.3% over the last six months while construction unemployment remains very low at 3.8%. Nationally, contractor confidence remains somewhat mixed in the industry for a third straight quarter.

While construction activity will remain strong for the balance of 2023, the forecast for 2024 calls for a pull back. The AIA/Deltek Architectural Billings Index has remained below 50 for all of 2023, and, given the 9-12 lead over construction spending, supports the forecast of declining spending starting in Q4 of 2023. The Commodore Builders Cost Index is still forecast at 6% for the year, which is higher than the 10-year average of 3-6% per year.

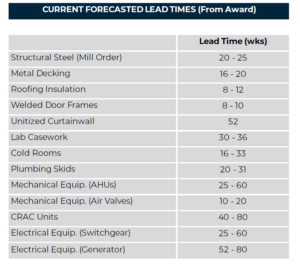

Supply Chain: Lead times for most materials and equipment continue to improve through Q3. However, certain products related to infrastructure, emerging technologies and green initiatives (transformers, generators, switchgear, metal sockets, bus plugs, & breakers) continue to have long lead times and higher prices. Despite the electrical industry adding 50%+ shipping capacity, market orders continue to outpace shipments by a factor of 1.5+ in many of these categories. This is driving the use of third-party brokers who have procured electrical & HVAC equipment from cancelled projects at pennies on the dollar, and are selling them at a market premium for projects which need to meet a schedule not otherwise feasible.

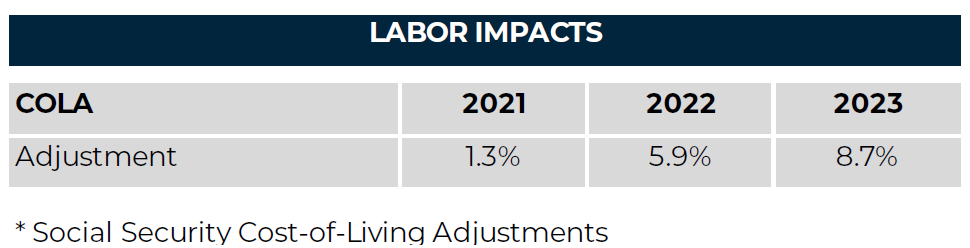

Labor Impacts:

Finding skilled labor continues to remain a major challenge for all aspects of the construction industry. Construction unemployment has been low since March 2022, and May 2023 was the lowest level yet (just 3.5%), which continues to drive construction wages higher. The construction employment cost index continues to rise, and is up to 4.6% through Q3 2023 which is 1.1% higher than the yearly average. As Federal interest rates continue to rise, this could begin to impact the labor market as projects might go on hold or even be canceled.

Risk Mitigation: Continued emphasis will be needed on project planning. Commodore Builders continues to focus on equipment pre-purchase / storage, realistic forecasting of material delivery to align with trade partner labor, and creative sourcing of alternate products to align with client scheduling needs. Driving collaboration with project team members will be crucial to the overall success of the project. Engaging with manufacturers to best understand procurement risks, accelerating submittals and approvals, and working with design partners to identify and source locally available materials and equipment are all keys to success. Aligning with trade partners earlier in the project to ensure labor demand is met can alleviate schedule risk. As contractors continue to experience market volatility, careful emphasis must be placed on trade partner prequalification to ensure no further risk in delivering a successful project.