Q2 2023 Market Update

MEET JIM STADLER, OUR PROCUREMENT EXPERT.

Jim is Vice President of Estimating and Purchasing at Commodore Builders. He brings over 20 years of experience working across all our markets including Life Sciences, Public and Municipal, Corporate Interiors, Commercial, and Institutional. His deep knowledge of costs during preconstruction planning helps to guide our teams through the cost planning process. Jim holds a B.S. in Civil Engineering from Norwich University.

Q2 2023 Market Analysis | Where we are today

Thanks to a strong economy, the construction industry continues to make gains and move forward despite lingering inflation.

While inflation has slowed from 9% in 2022 to around 4% currently, economists predict the economy hasn’t slowed down enough for the Fed’s liking and interest rates will be increased once more before the end of 2023. While most predict that a recession is unlikely, another interest rate increase could add pressure to the construction industry and the economy as a whole. According to the American Institute of Architects (AIA) Consensus Forecast Panel, spending on (non-residential) buildings has increased by 20% in 2023 but will begin to moderate in the second half of the year and into 2024. The market that bolstered this growth is primarily manufacturing (projected 50% increase YoY), but modest gains were experienced in other sectors including infrastructure, private institutional, public educational, and healthcare.

The AIA/Deltek Architecture Billings Index is the leading indicator on where the construction market is headed based on design activity. The typical lag from design activity to construction spending is approximately 9-12 months. In Q1/Q2 of 2022, the index averaged 53.6, but by Q4 it had declined to 48.1. At no point in 2023 has the index measured over 50. Based on this data, construction spending is expected to moderate in Q3 and decline in Q4 through the first half of 2024.

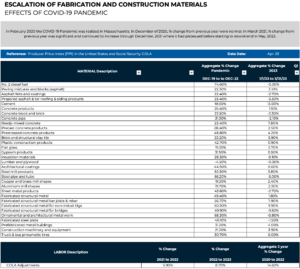

Supply Chain: In Q2, lead times for many items have stabilized with opportunities for shorter durations to be found with alternate domestic manufacturers in many cases. Like in previous quarters since the pandemic began, electrical distribution equipment continues to be a challenge, particularly on larger scale switch gear packages, pad mounted equipment, breakers, sockets, bus plugs, and generators. Conversely, shipping rates have decreased to pre-pandemic levels, congestion in ports is easing, and the overall freight costs are down between 15 & 20% YOY.

Material Costs: Apart from a few outliers (Concrete & Steel), the PPI continues to show signs of stabilization through Q2. In general, construction material costs are still higher YOY than Q2 2022, but the trend has slowed significantly, with the expectation that we will see fewer fluctuations in commodities for the remainder of the year. For the outliers previously mentioned, steel is anticipated to increase up to 10%, and concrete up 9.5% through Q2 due to raw material shortages. These will also be joined by glass in Q3 as raw materials shortages, increased demand, and manufacturing constraints continue to put a strain on the market. There is concern over lumber prices in the future due to the forest fires in Canada, and the potential for production to decline as a result – pushing up prices in the second half of 2023.

Construction Escalation: In 2022, construction escalation in the Boston market was 9% according to ENR. Only slightly lower than 2021’s level of 9.5%. As we reach the mid-point of 2023, the PPI has stabilized with only a few outliers, while labor costs continue a steady upward trend, yielding a 2.9% construction cost increase for the first half of the year. While these values are trending slightly higher than the 2.5% – 4% YOY averages seen over the last decade, they are less than the increases of 2021 & 2022. Our forecast remains at 6% for the year.